Namu | 나무 개발자 블로그입니다

[번역] SOFI: Back To Where It Started by namu

[참조링크] SOFI: Back To Where It Started

SOFI: Back To Where It Started

SOFI, 시작점으로 돌아가다

Summary

- SoFi is cheap with the stock trading at the de-SPAC lows

- The fintech continues to make great progress towards approval on the bank charter that will save up to 200 basis points on loan costs and improve revenues

- The stock is too cheap trading at ~10x original ‘24 adjusted EBITDA targets.

- Looking for more investing ideas like this one? Get them exclusively at Out Fox The Street. Learn More

- SoFi 는 스팩 합병(de-SPAC) 시점의 최저점만큼 저렴합니다.

- 이 핀테크 기업은 대출 비용을 최대 200bp(basis point)만큼 절감하고 수익을 향상시킴으로써 은행 헌장(bank charter) 승인을 향해 지속적으로 훌륭한 진전을 이루고 있습니다.

- 이 주식은 당초 ‘24 조정 EBITDA(‘24(년도) 조정 운영이익) 목표치의 1/10수준으로 매우 저렴합니다.

- 이와 같은 투자 정보를 더 많이 찾고 있습니까? Out Fox The Street 에서 독점적으로 얻어보세요! 더 알아보기

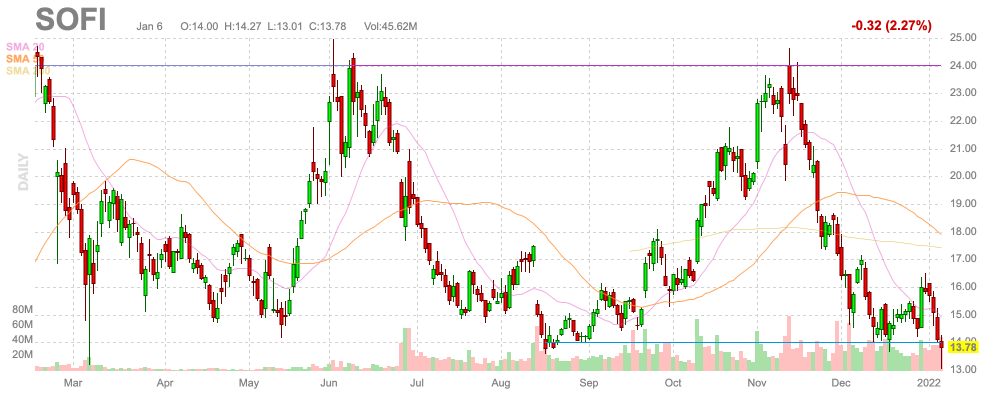

Despite a very promising start, SoFi Technologies(SOFI) now trades back to where the stock traded at the time of the de-SPAC transaction last May. The fintech super app was a buy the last couple of times the stock fell below $15 and nothing has changed now. My investment thesis remains Bullish on SoFi now down at $13 following a nearly 50% dip after multiple trips above $24.

매우 안정적인 시작에도 불구하고, 현재 소파이 테크놀로지(SOFI)는 지난 5월인 스팩 합병전환 시점에 거래되었던 가격으로 회귀해 거래되고 있습니다. 이 핀테크의 수퍼앱은 지난 몇 번 $15 아래로 떨어진 가격에 거래되었고 현재도 변한 것이 없습니다. 저의 투자 기고문 은 여러 번 $24 수준으로 올라갔다가 현재 50% 가까이 하락하며 $13 대로 떨어진 소파이에 대해 여전히 긍정적인 의견을 유지하고 있습니다.

Not Perfect

SoFi hasn’t had a perfect history as a public company. The fintech came out of the gate reporting Q3’21 revenue targets far below analyst expectations at the time: $250 million versus $270 million.

소파이는 공개된 기업으로써 완벽한 역사를 가지고 있지는 않습니다. 이 회사는 당시 애널리스트의 기대치를 훨씬 밑도는 수준의 21년 3분기 수익 목표치 를 보고했습니다. (애널의 기대치는 $270 million 이었으나 기업의 보고치는 $250 million 이었음)

The company ultimately reported revenue of $272 million, actually topping the original analyst estimate. SoFi smashed both analyst revenue and EPS estimates sending the stock back to previous highs at $24.

이 회사는 궁극적으로 $272 million 의 수익을 보고 함으로써, 당초 애널리스트의 추정치를 실제 능가하였습니다. 소파이는 애널의 수익과 EPS 추정치를 모두 깨고 주가를 이전의 최고점인 $24 로 되돌려놓았습니다.

The fintech has seen both Members and Products nearly double YoY. The business saw accelerated growth in people joining the platform and the products used by customers with the peak growth at 123% growth in Q2’21. SoFi has maintained 100%+ growth in Products for the 5th consecutive quarter in Q3’21.

이 핀테크 기업은 가입자수와 제품수 모두 작년 동기 대비(YoY) 두배가 되는 모습을 보였습니다. 이 비즈니스는 플랫폼에 참여하는 사람들과, 123% 로 21년 2분기 가장 높은(peak) 성장을 나타내는 고객 사용 제품 면에서 가속화된 성장을 보이고 있습니다. 소파이는 21년 3분기 5분기 연속 100%가 넘는 제품 성장을 유지하고 있습니다.

Amazingly, due to interest rate fears, the stock is actually right back to the lows where SoFi traded after originally guiding down Q3’21 targets. The company guided to solid Q4’21 revenue $277 million and 2021 revenues topping $1 billion despite major headwinds. The fintech estimated a $52 million negative impact from the CARES Act extension on SLR volumes and the equity investment in Apex being called earlier last year.

놀랍게도 금리(인상)에 대한 두려움으로 인해 이 주식은 원래 21년 3분기 목표치를 햐향 조정한 이후에 소파이가 거래되던 낮은 지점으로 되돌아가고 있습니다. 이 회사는 주요한 역풍에도 불구하고 21년 4분기 $277 million 고정 수익과 2021년 $1 billion 으로 달성된 수익을 안내하였습니다. 그리고 SLR 볼륨에서 the CARES Act 연장으로부터의 부정적인 영향을 $52 million 으로 추정했으며, 작년 초 Apex 에서의 지분 투자가 요청되었습니다.

Even the bank accounts on the Galileo financial platform continue to grow at a fast clip reaching 89 million client-enabled accounts in the last quarter. SoFi only had 25 million accounts on the fintech technology platform at the end of 2019.

Galileo 금융 플랫폼의 은행 구좌가 지속적으로 빠르게 성장하면서 지난 분기 클라이언트 사용 계정이 8천 9백만에 달했습니다. 소파이는 2019년말 금융 기술 플랫폼에서 단지 2천 5백만의 계좌를 보유하고 있었습니다.

In general, the issues faced by SoFi in the last year were mostly related to timing issue on revenues due to COVID-19 related impacts. As far as new Members and Products, the fintech executed on every level creating a one-stop financial product for customers. The growth was focused on SoFi Invest and SoFi Money offerings while consumers are less in need of lending products due to government programs.

일반적으로, 소파이가 작년에 당면한 이슈들은 대부분 수익 면에서 COVID-19 관련 효과로 인한 타이밍 이슈에 연관되어 있었습니다. 이 핀테크 기업은 새 멤버와 상품들까지 포함하여 고객들을 위한 one-stop 금융 상품의 출시(creating)를 모든 레벨에서 실행했습니다. 이 성장은 소파이의 투자와 자금 제공에 초점이 맞춰져 있는 반면 소비자들은 정부 프로그램으로 인해 대출 상품의 필요가 더 적었습니다.

While all of these numbers are impressive for the future, SoFi still obtains the majority of quarterly revenues from their lending products.

이러한 모든 수치는 미래적인 관점에서 인상적이지만, 소파이는 여전히 그들의 대출 상품으로부터 분기별 수익의 대부분을 얻고 있습니다.

Adjusted net revenue in the lending category was $215 million, or ~78% of total revenues. Assuming the government stops pushing back the moratorium on student loan payments beyond May 1, SoFi should see a faster growth in revenues later this year.

대출 카테고리에서의 조정된 순수익(net revenue)은 $215 million 로, 전체 수익의 78% 수준입니다. 정부가 만약 학자금 대출 지급에 대한 지불중지를 5월 1일 이후로 연기하는 것을 중지한다고 가정하면, 소파이는 올해 말 수익 면에서 더 빠르게 성장할 것입니다.

Waiting On Bank Charter

Considering the dependence on capital to finance their lending products, the pending bank charter is crucial to the long term success of SoFi. The fintech needs bank deposits from Members in order to fund future loans similar to traditional banks.

그들의 대출 상품들이 재원을 확보하기 위해 자본에 의존하는 것을 고려하여, 연기되고 있는 은행 헌장(bank charter)은 소파이의 장기적인 성공에 있어서 결정적입니다. 핀테크 기업은 전통적인 은행들과 유사하게 미래의 대출 자금을 마련하기 위해 고객들로부터의 은행 예금이 필요합니다.

At the recent Credit Suisse Technology conference, CFO Chris Lapointe repeated the benefits of the bank charter the company is optimistic at obtaining full approval:

In terms of the benefits of having a bank charter, right now, it comes in multiple fold, primarily it’s a cost of capital play and will allow us to grow our lending business in a more robust way. So to give you a little bit of context, our lending business, right now, we rely on about $6 billion of warehouse capacity, as well as our own equity capital in order to fund originations. So we originate loans, we fund them with warehouse capacity. And historically, we’ve paid anywhere between 175 to 400 basis points in terms of cost of capital… So think of this as if we’re paying 300 basis points on warehouse facility but we offer 1% interest rate to our SoFi Money members, we’re able to save 200 basis points in terms of origination costs for our lending business, which is quite significant.

최근의 Credit Suisse 기술 컨퍼런스에서, CFO Chris Lapointe 는 은행 헌장의 이점과 회사는 충분한 승인을 얻는 데 낙관적이라고 반복해서 이야기했습니다:

은행 헌장을 얻는 것의 이점의 측면에서, 지금 당장에 그것은 우선적으로 자본 융통의 비용 그리고 더욱 강력한 방식으로 우리의 대출 사업을 성장시킬 수 있도록 하는 등 여러 가지로 다가올 것입니다. 또한 지금 당신에게 우리의 대출 사업에 대한 약간의 맥락을 제공하기 위해 설명하자면, 우리는 자금을 마련하기 위해 $6 million 의 은행 자본(웨어하우스 자본)과 자체 자기 자본에 의존하고 있습니다. 따라서 우리는 대출을 개시하고, 은행 자본(웨어하우스 자본)으로 그것들에 자금을 조달합니다. 그리고 역사적으로 우리는 자본 비용의 측면에서 1.75% ~ 4%(175bp to 400bp) 사이의 비용을 지불해 왔습니다 … 따라서 이것을 마치 은행(웨어하우스) 시설에 3%(300bp) 를 지불하는 것으로 생각될 수 있지만 소파이 머니 고객들에게 1% 이자율을 제공한다고 생각해 보면, 우리는 우리의 대출 사업의 개시 비용 측면에서 2%(200bp) 만큼을 절감할 수 있습니다. 이것은 매우 의미 있는 일입니다.

In essence, SoFi is able to pay 100 basis points to Members for cash deposits versus the 300 basis points on a warehouse loan. The fintech won’t face the same risks of lending capacity shrinking during financial crisis and the company will save 200 basis points on costs. Also, SoFi can hold onto loans for a longer period of time to generate more interest income versus a current period of only up to four months.

본질적으로, 소파이는 현금 예금을 한 사용자들에게 100bp를 제공할 수 있는 반면 은행(웨어하우스) 대출에 대해서는 300bp를 제공할 수 있습니다. 이 핀테크는 금융 위기에도 대출 자본이 축소되는 동일한 위험에 직면하지 않을 것이며, 200bp 의 비용을 절감할 것입니다. 또한, 소파이는 현재 최대 4 개월에 불과한 기간보다 더 많은 이자 수익을 생성하기 위해 더 긴 기간 동안 대출을 보유할 수 있습니다.

The current consensus analyst estimates already have revenues rising to nearly $1.5 billion next year and nearly $2.1 billion in 2023. The company has very attractive growth rates even before the addition of the bank charter.

현재의 애널리스트 평가의견은 이미 다음년도의 수익은 $1.5 billion 에 달할 것이고, 2023년에는 $2.1 billion 에 이를 것으로 추정하고 있습니다. 이 기업는 심지어 은행 헌장을 추가하는 것 이전에 이미 매우 매력적인 성장률을 보유하고 있습니다.

At the time of the SPAC deal, SoFi predicted up to $234 million upside to 2034 EBITDA from the bank charter. The stock has a market cap of $11 billion with an enterprise value down around $8 billion based on over $3 billion in financial assets from cash and net loans on the balance sheet. Anything close to the previous 2024 adjusted EBITDA targets of $1.05 billion places SoFi at a very attractive valuation with the stock down at the lows.

스팩 거래가 진행되는 시점에 소파이는 은행 헌장으로부터 2034년 EBITDA 까지 $234 million 의 업사이드가 예견되어 있었습니다. 이 주식은 $11 billion 의 시가총액을 보유하고 있으며 기업 가치는 대차대조표상 현금과 순수 대출로 인한 $3 billion 이상의 금융자산 기준 $8 billion 정도 하락했습니다. 앞선 2024년도 조정 EBITDA 목표치인 $1.05 billion 지점에 도달하게 된다면 소파이는 매우 매력적인 밸류에이션과 함께 주가가 최저점에 도달하게 됩니다.

Takeaway

The key investor takeaway is that SoFi is far too cheap down at the lows. The fintech has a major catalyst in an already fast growing business, yet the stock trades as if the business has been impaired. The stock is now trading around 10x original 2024 EBITDA targets, assuming the bank charter is approved. Investors should buy the stock ahead of the bank charter approval and before the moratorium on student loans expires allowing their lending business to return to normal.

투자자가 가져갈 핵심은 소파이가 최저점인 너무 싼 가격에 내려왔다는 것입니다. 이 핀테크는 이미 빠르게 성장하고 있는 비즈니스에서 주요한 촉매제를 가지고 있으면서도 마치 비즈니스가 손상된 것처럼 주식이 거래되고 있습니다. 주가는 은행 헌장이 승인되었다는 가정 하에 본래 2024 EBITDA 목표치 대비 약 10배의 가격으로 거래되고 있습니다. 투자자들은 은행 헌장이 승인되기에 앞서 그리고 기업의 대출 사업이 정상으로 돌아가도록 하는 학자금 대출 지불 중지(모라토리움)가 만료되기 이전에 매수해야만 합니다.

Written on January 9th, 2022 by namu